Global Shrimp Market 2025 Overview

According to Shrimp Insights' Shrimp Bulletin #02 (February 2026), 2025 saw a major restructuring of global shrimp trade flows. US tariffs, new trade agreements, and Indonesia's Cesium-137 incident reshaped import-export dynamics worldwide.

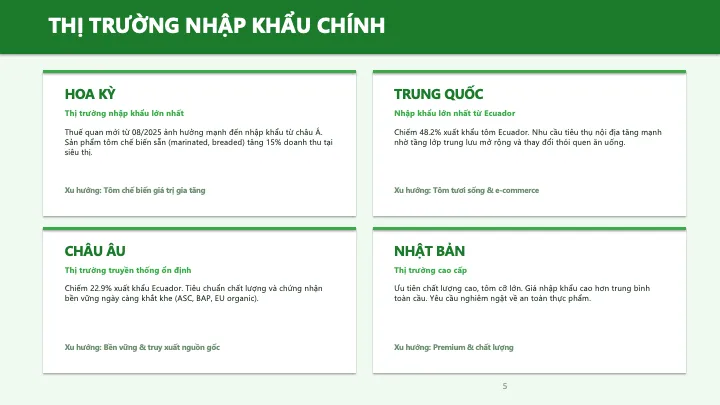

Key Import Markets

China — 901,563 MT (-2% YoY)

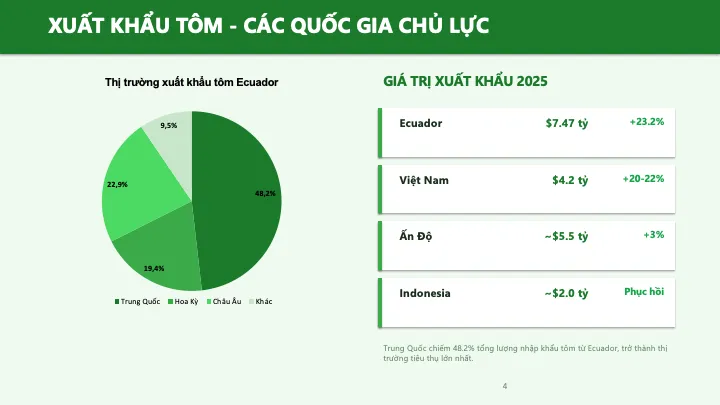

China's shrimp imports declined slightly in volume but rose 5% in value to $4.79 billion. Ecuador remained the primary supplier at 651,866 MT (-3%), while India accelerated to 149,599 MT (+6%), with P. monodon exports doubling. Indonesia (+28%) and Argentina (+10%) also expanded their footprint.

USA — 795,641 MT (+2% YoY)

The US market showed a clear two-phase year: strong H1 growth (June peak +35%), followed by sharp H2 decline due to tariff impacts. Total value reached $7.03 billion (+9%).

- India: #1 supplier at 300,051 MT (+1%), but Q4 collapsed (Oct -57%)

- Ecuador: Biggest winner at 231,804 MT (+18%), surging from September

- Indonesia: Down 11% (119,331 MT) due to Cesium-137 incident, but December recovered

- Vietnam: Down 7% (64,413 MT), Thailand: Down 4% (26,958 MT)

EU-27 — 455,776 MT (+21% YoY) — Strongest Growth

The EU was the standout import market in 2025. Import value reached €2.87 billion (+22%). Growth was consistent throughout the year with Q4 particularly strong.

- Ecuador: 241,947 MT (+35%) — dominant supplier

- India: 66,843 MT (+44%) — strongest growth as volumes diverted from US. December surged +113%

- Vietnam: 57,758 MT (+14%) — steady, leading cooked-at-origin segment

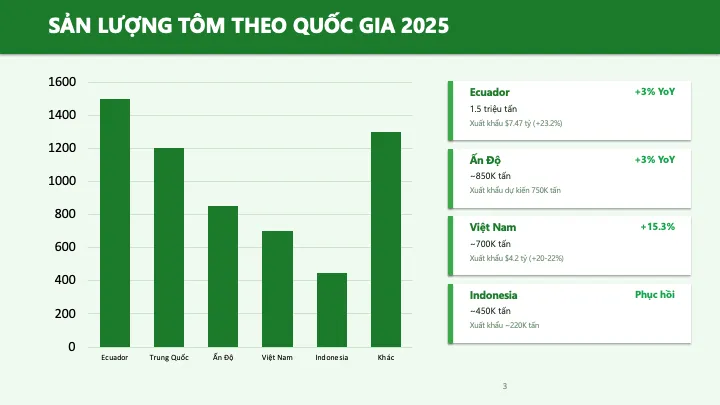

Major Exporting Countries

Ecuador — 1.39M MT (+15%), $7.48B (+23%)

Ecuador confirmed its global leadership. Top exporters: Santa Priscila (25%), Omarsa (10%), Songa, Aquagold, Exportquilsa (~5% each). Q1/2026 forecast: +10-11% YoY, with January reaching ~118,000 MT (+15%, all-time record).

India — 796,374 MT (+9%), $5.66B (+14%)

India aggressively diversified away from the US (-9%) toward EU (+39%), China (+10%), and Vietnam (+61%). P. monodon surged 36% to 56,587 MT. 2026 outlook: L. vannamei stocking delayed 1 month; P. monodon forecast lowered to ~100K MT.

Indonesia — 201,113 MT (flat), $1.78B (+11%)

Highly volatile year. Strong H1 followed by Q4 collapse due to Cesium-137 case (October -59%). December recovered +31%. US FDA rejected 30 Indonesian shrimp entry lines in 2025 for banned antibiotic residues.

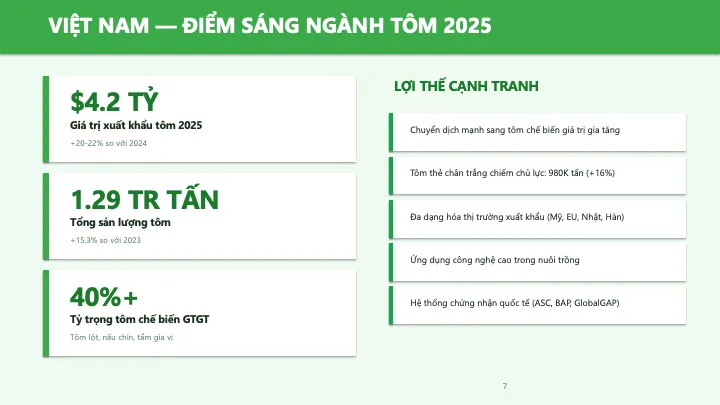

Vietnam — 275,530 MT (+3%), $2.21B (+9%)

Gradual recovery with value-added products as the growth engine (+12%). Record import of 99,000 MT raw material (75% from India) for reprocessing. Anti-dumping duties: STAPIMEX/Thong Thuan at ~25.8%, other exporters at ~4.6%.

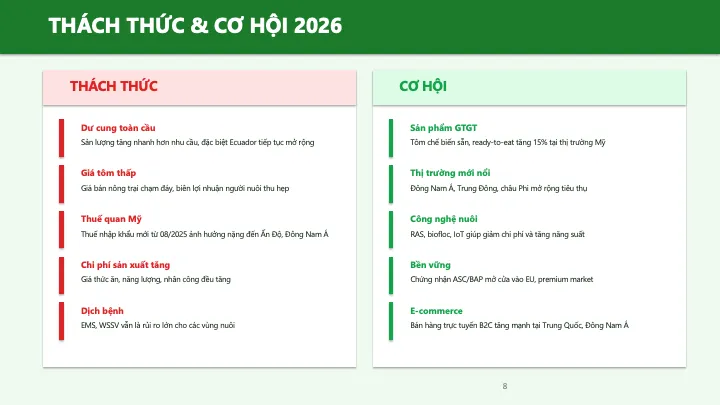

Trade Policy Developments

- US Supreme Court struck down IEEPA tariffs (Feb 2026): Temporary Section 122 tariffs at 10% moving to 15%

- US-India interim deal: Reduced Indian shrimp tariff from 50% to 18%

- EU-India FTA signed Jan 27, 2026: Expected in force early 2027

- EU antibiotics regulation (Reg. 2024/2598): India, Indonesia not listed — risk of losing EU access from Sep 2026

- US FDA 2026: Enhanced imported shrimp oversight with expanded sampling and traceability

Source: Shrimp Insights — Shrimp Bulletin #02, February 2026. Data from Customs (China), NOAA (USA), Eurostat (EU), CNA-Ecuador, Ministry of Commerce India, Bureau of Statistics Indonesia, Customs Vietnam.